Indicators

The contracts entered into by Banrisul, and its associate companies focus on the appropriate treatment of their technical staff, who has a direct role in the provision of services. The contractor is responsible for ensuring this appropriate treatment, while the Bank assumes joint responsibility for supervising these practices, complying with state laws and the Federal Constitution. All contracts have provisions on social criteria, and all contracts entered into by Banrisul have specific clauses related to labor and social issues, in compliance with the specific legislation.

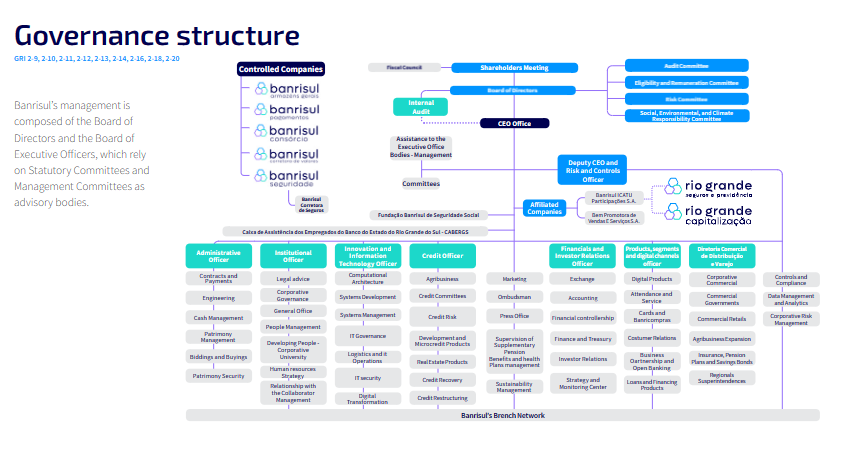

After the Management Proposal is published, the shareholders make nominations for the Board of Directors, which are subsequently submitted to the Chief of Staff of the Government of the State of Rio Grande do Sul for approval. If the nominations are approved, their names and information will be forwarded to the Treasury Department for the opening of an administrative proceeding via the PROA system. Upon the receipt of the Administrative Proceeding, the Eligibility and Compensation Committee analyzes the nominee, taking into consideration the eligibility requirements outlined in the Nomination and Succession Policy, which determine that the background and experience of the nominees for the Board of the Directors should be assessed, as well as their time availability to perform the duties, diversity, knowledge, experience, behavior, cultural aspects, age group, and gender. The Committee’s opinion is forwarded to the State Attorney General’s Office for a final decision about the fulfillment of the requirements and the absence of impediments. Once the nomination has been approved by the State Attorney General’s Office, the proceeding returns to the Company, so that the election can be held.

Every two years, before the Annual and Extraordinary Shareholders’ Meeting, shareholders submit their candidates for the highest governance body. The controlling shareholder makes its nominations considering the criteria set forth in the current legislation (Federal Law 13,303/16; Federal Law 6,404/46 and State Decree RS 54,110/18).

In 2022, the Nomination and Succession Policy was updated and stated that the election of Banrisul’s Board of Directors members, should include seats for Diversity groups as of 2023, as follows: I – the shareholder, or group of shareholders, with a right to nominate 25-40% of seats on Banrisul’s Board of Directors, shall be responsible for allocating at least one of the openings for members of the Diversity group; II – the shareholder, or group of shareholders, with a right to nominate for Banrisul’s Board of Directors any percentage higher than that established in item I must allocate two or more openings for members of the Diversity group; III – Grupo Banrisul must adjust the composition of the Boards of Directors, which shall respect the minimum percentage of 30% for openings aimed at the Diversity group, by 2030.

Independence criteria must also be considered, as provided for in article 22 of the Bylaws, which can be read here.

Banrisul’s current eligibility process involves several spheres (State Department of Finance, State Chief of Staff and State Attorney General’s Office, among others). This verification flow conveys security and reliability to all stakeholders.

For the unbanked public involved in financial education strategies, the engagement numbers were as follows:

| Public | Participations | |

|---|---|---|

| 2021 | 2022 | |

| Projeto Pescar | 40 | 40 |

| Jovem Aprendiz | 20 | 70 |

| Students | - | 116 |

| Nova Geração Caldeira | - | 50 |

No potential risks of child labor or young workers exposed to hazardous work were identified in the Institution’s operations.

Suppliers, especially those with contracts involving the outsourcing of labor, are submitted to thorough checks for compliance with labor and social security obligations, monitoring certificates of good standing, among other actions.

Regarding customers, Banrisul conducts checks to make sure they have all applicable certificates and licenses, in addition to assessing their history of non-compliance.

No potential risks for incidents of forced labor were identified in the Institution’s operations.

As for suppliers, Banrisul closely supervises compliance with labor and social security obligations through the monitoring of certificates of good standing, among other actions.

Customers are checked against a list of employers of who use compulsory labor published by the Ministry of Labor and Employment.

According to Banrisul’s Anti-Corruption Policy, all those subject to the Policy are responsible for fostering an ethical culture and for creating an environment of permanent corruption control and prevention, in which it is possible to monitor and identify, through Due Diligence procedures, operations from customers and non-customers – individuals and companies – and actions or suspected corruption crimes, as well as enforcing the internal integrity and auditing mechanisms and procedures, encouraging whistleblowing and the effective application of Banrisul’s Anti-Corruption Policy and Code of Ethics and Conduct.

Moreover, in 2021, a Social, Environmental and Climate Risks (RSAC, in Portuguese) assessment questionnaire was developed for operations over R$10 million, which includes anti-corruption questions.

Operational risk management includes identifying and assessing external fraud events, the possibility of employee misconduct that offers or results in undue advantage and operational flaws in developing processes to assess or identify suspicious operations.

The Bank is subject to Brazilian and foreign anti-corruption legislation. These laws require the adoption of integrity procedures in order to mitigate the risk that any person, acting on behalf of the Bank, may offer an undue advantage to a public agent, in order to obtain benefits of any kind. The transnational scope legislations, including, but not limited to, the U.S. Foreign Corrupt Practices Act of 1977 and the UK Bribery Act of 2000, in addition to Federal Law no. 12,846/13, provide for the adoption of specific policies and procedures for the prevention and fight against illegal acts related to corruption of public administration entities and government representatives, which aim at ensuring any kind of advantage. They also require the Bank to keep its books and records accurate and rely on an internal controls system to certify their respective veracity, in addition to the prevention of illegal activities.

There is no percentage of assets subject to positive or negative social or environmental screening.The Agribusiness Department does not use screening criteria. However, before contracting a transaction, the department runs a social and environmental compliance check to verify social issues (forced labor, IBAMA and ICMBio embargoes, administrative improbity and ineligibility) and environmental issues (overlap of the area to be financed with land reform settlement areas, indigenous land, quilombola territory, conservation units, areas embargoed by IBAMA or ICMBio, areas susceptible to flooding, archaeological sites and areas with deforestation alerts. Moreover, in order to grant rural credit, the Bank requires environmental licensing of the financed activity.

| Performance Assessment per Category³ | 2020 | 2021 | 2022 | |||

|---|---|---|---|---|---|---|

| Men | Women | Men | Women | Men | Women | |

| Managers¹ | 23.7% | 38.7% | 21.6% | 36.0% | 25.6% | 41.3% |

| Supervisors | 62.2% | 76.4% | 60.6% | 72.2% | 59.2% | 71.3% |

| Total² | 31.4% | 48.5% | 28.9% | 44.1% | 31.2% | 47.3% |

¹ It includes the following employee categories: account manager, market manager, agribusiness relationship manager and business manager (corporate, other states and government).

² It considers all of the Company’s employees.

³ Only those categories that receive performance and competence assessments as a result of the in-house training courses specified in note 1 were taken into account.

The Institution is grounded on its values defined in its Code of Ethics as transparency, ethics, commitment, integration and efficiency, as well as in principles and guidelines, such as integrity, respect for diversity, people, appreciation of work, social and environmental responsibility, respect for competition, respect for the image and excellence in rendering services.

The commitments refer to internationally recognized intra-governmental instruments, namely the Brazilian Central Bank, Febraban, National Monetary Council, UN Global Compact Guidelines and SDG 16.

These guidelines/policies set forth responsibilities and consequences for all levels.

Banrisul manages capital and credit, market, interest rate variation risks for the instruments classified in the banking portfolio – IRRBB- in a continuous and integrated manner; as well as liquidity, operational, social, environmental, climate and other risks considered relevant.

Social risk, defined as the possibility of the Institution incurring in losses from events related to the violation of fundamental rights and guarantees or by acts that are harmful to the common interest, is one of the relevant risks included in the Risk Management Policies.

Banrisul does not have a specific human rights policy.

Human rights are rules that recognize and protect the dignity of all human beings and govern how individual human beings live in society and among themselves, as well as their relationship with the State and the obligations that the State has in relation to them. In this regard, as a signatory to the Global Compact since 2013, Banrisul reaffirms its commitment to the well-being of its employees, as well as to seeking to ensure the rights of its customers, suppliers and all stakeholders to which it engages. The Bank manages social risk, particularly, in order to mitigate possible actions that may occur under the human rights aspect.

The stakeholder categories to whom the Organization pays special attention in this commitment are employees, customers, suppliers and vulnerable publics.

Policy commitments should be approved by the Board of Directors. These commitments apply to management members, board members, employees, interns, members of the Banrisul Group, business partners, suppliers and the Group’s service providers.

An Administrative Instruction is issued stating that all employees must sign a Compliance Agreement, which is published in the Institutional Manual (Chapter 04 of Banrisul’s Code of Ethics and Conduct).

All employees receive training on the Code of Ethics and Conduct and the Anti-Corruption Policy. Banrisul has other institutional policies and makes a whistleblowing channel available both on the internal and external websites. The commitments of the Code of Ethics and the Anti-Corruption Policy are available to the public.

In 2022, Banrisul conducted a complete materiality assessment to define its material topics, which encompassed peer benchmarking, as well as analysis of the Company’s internal documents and industry literature, such as ESG ratings and standards. A list of material topics for the industry was prepared based thereon. This list was discussed and validated with important stakeholders through interviews (the CEO, Sustainability Corporate Department and Executive Board) and, then it was prioritized through an online survey with a larger stakeholder group.

At the same time, based on the analysis of internal risk documents, the Company assessed possible impacts related to each topic, which were duly classified as regards their nature and then added to the consolidated materiality results.

Results were assessed using a methodology that weighted the answers according to each stakeholder group. The results of the online survey were consolidated to the topics’ impact study to prepare the final list of material topics.

A total of 1,315 people from the following stakeholder groups participated in the online survey:

- Employees;

- Shareholders/investors (priority);

- Shareholders/investors (diversified);

- Capital markets;

- Customers;

- Main suppliers;

- Government;

- Representatives of non-profit organizations and/or social institutions;

- Specialized media outlets;

- Union representatives;

- Executive Officers;

- Board of Directors members;

- Sustainability Committee members.

Prioritization and final approval:

Sustainability Corporate Department, CEO and Administrative Executive Board. The materiality results were also presented to the Sustainability Committee, the Social, Environmental and Climate Responsibility Committee and the Executive Board.

The responsibilities of the Eligibility and Compensation Committee are:

(i) drafting the compensation policy for Management of the Bank and its subsidiaries, suggesting to the respective Boards of Directors various forms of fixed and variable compensation, in addition to benefits and special recruiting and severance programs;

(ii) proposing to the Boards of Directors of the Bank and subsidiaries the overall Management compensation amount to be submitted to the respective Shareholders’ Meetings, pursuant to Article 152, of Law 6,404, of 1976;

(iii) assessing future internal and external scenarios and their possible impacts on the Management compensation policy of the Bank and its subsidiaries;

(iv) analyzing the Management compensation policy of the Bank and its subsidiaries vis-à-vis market practices in order to identify significant discrepancies compared its peers, proposing the necessary adjustments.

As per CMN Resolution 3,921/10, the Eligibility and Compensation Committee is responsible for assisting in the process of determining compensation. The Committee is composed of three independent members, all of whom are natural persons residing in Brazil, with higher education degrees and technical skills suitable for the position they hold. The members also meet the criteria for holding positions in statutory bodies of financial and other institutions authorized to operate by the Brazilian Central Bank.

The board members convene in ordinary and extraordinary meetings, and their considerations are recorded in minutes. In turn, shareholders can express their opinions at the Annual/Extraordinary Shareholders Meeting.

The Board of Directors members are only entitled to fixed monthly compensation as fees, and are not entitled to variable compensation or direct and/or indirect benefits. Executive Board members are entitled to monthly compensation in the form of monthly wage plus a representation fee, the annual amount of which must not exceed the overall management compensation amount set by the Extraordinary and Annual Shareholders’ Meeting. They are also entitled to Banrisul’s Profit Sharing Program (PLR, in Portuguese), calculated in accordance with the rules established by the Board of Directors, considering the rules applicable to the payment of PLR to employees, as defined in the Banking Employees’ Collective Bargaining Agreement. In addition to the PLR, the Banrisul Conglomerate may pay variable compensation to its executive officers, provided it is included in the overall compensation approved by the Shareholders’ Meeting, observing the limits established by the legislation in force and based on criteria that may be defined by the Board of Directors.

The report is published every year and this reporting period is between January 1, 2022 and December 31, 2022.

Contact: Sustainability Corporate Department, Rua Caldas Júnior, 108, 6º andar

E-mail: Sustentabilidade@banrisul.com.br

No information has been restated in previous reporting periods.

The composition of the Board of Directors ensures a seat for common minority shareholders, preferred minority shareholders and a representative of the employees, who is chosen by internal election, according to the Board of Directors Charter. Thus, stakeholder groups are engaged in the Board of Directors meetings.

The Board of Directors is responsible for the Company’s overall direction of business, institutional guidelines and goals. As regards Integrated Capital and Corporate Risk Management, the Board is responsible for:

a) Establishing the Institution’s risk appetite levels in the Risk Appetite Statement (RAS) and reviewing them supported by the Risk Committee, the Executive Board and the Chief Risk Officer (CRO);

b) Ensuring compliance with the Institution’s policies, strategies and risk management limits;

c) Whenever necessary, authorizing exceptions to policies, procedures, limits and risk appetite levels set out in the RAS;

d) Ensuring that the Institution’s compensation structure does not encourage behaviors that are incompatible with risk appetite levels set out in the RAS;

e) Ensuring that the Institution keeps adequate and sufficient capital and liquidity levels;

f) Having a broad and integrated knowledge of risks that can hinder capital.

As for Corporate Risk Management, the Board of Directors, the Risk Committee, the CRO and the Executive Board have seral joint responsibilities, including:

a) Understanding, in a broad and integrated way, risks that can impact the Institution’s capital and liquidity;

b) Understanding the limits of information included in capital and risk management reports;

c) Ensuring that the Institution complies with the content of the RAS;

d) Understanding the limits and uncertainties related to the assessment of risk models, even when they are developed by a third party, and the methodologies used in risk management structure; and

e) Ensuring the Institution’s different levels understand and continually monitor risks.

The Board of Directors meets periodically to evaluate changes to the capital and corporate risk management policies, as well as management reports on the main risks to which the Institution is exposed. At Management level, Banrisul relies on the Corporate Risk Committee and the Control and Risk Executive Office and, statutorily, on the Statutory Risk Committee.

In compliance with CMN Resolution 4,945, of September 15, 2021, Banrisul’s Social, Environmental and Climate Responsibility Policy (PRSAC, in Portuguese) determines that it is incumbent upon the Executive Board, a governance body elected by the Board of Directors, to:

a) provide input and participate in the decision-making related to the drafting and review of the PRSAC, assisting the Board of Directors;

b) support the implementation of actions to ensure this Policy’s effectiveness;

c) monitor and evaluate implemented actions;

d) ensure that implemented actions are improved whenever possible deficiencies are identified;

e) help and encourage the adequate and reliable dissemination of mandatory information;

f) manage the PRSAC at Banrisul. The responsibilities of the Board of Directors include ensuring that the Institution complies with the PRSAC and taking measures to ensure its effectiveness.

Banrisul has a the Social, Environmental and Climate Responsibility Committee (CRSAC, in Portuguese), an advisory body to the Board of Directors, whose duties and responsibilities are to:

a) make recommendations to the Board of Directors on the drafting and review of the Social, Environmental and Climate Responsibility Policy;

b) evaluate if the actions implemented are in compliance with the Social, Environmental and Climate Responsibility Policy and, whenever necessary, make recommendations for improvement;

c) keep records of its deliberations and decisions;

d) evaluate and monitor the Bank’s sustainable performance and the effectiveness of the actions laid down in the Sustainability Plan;

e) monitor advancements in sustainability, seeking to identify opportunities and risks, in order to create value for the Bank and its stakeholders;

f) propose and follow-up the execution of initiatives that improve the Bank’s socio-environmental performance;

g) assisting the Board of Directors in incorporating sustainability into the Company’s business strategy and administrative practices and follow up its progress;

h) analyze, monitor and issue recommendations and opinions to support the Board of Directors’ decisions on policies and practices related to its field;

i) fulfil other duties determined by the Board of Directors.

The Message from the CEO can be found in the Sustainability Report on page 4.

The Ombudsman’s Office classifies the complaints received by its channels into topic, item and root cause. Regarding subject, there is a “bank secrecy” item, which is under the topic “other subjects” and the root cause “LGPD” (Brazilian General Data Protection Law). In 2022, five customer complaints were filed related to bank secrecy and/or LGPD, including in external agencies; four of these complaints were classified as invalid and only one was classified as valid (not resolved). In the latter, there was proof of a data breach.

The report classified was valid was received through the Consumer Protection Agency (Procon, in Portuguese)/RS (external agency).

| Waste generated by type and destination (t) | |||

|---|---|---|---|

| 2020 | 2021 | 2022 | |

| Hazardous waste (Class I) - diverted from disposal | |||

| Batteries- Recycling | 0 | 0 | 0,1 |

| Non-hazardous waste (Class II) - diverted from disposal | |||

| Banners, shredded cardboard and acrylic - Recycling | 0 | 2,8 | 0 |

| Structured network cables - Reverse logistics | 0 | 0 | 0,1 |

| Vaults - Recycling¹ | 0 | 10,4 | - |

| Electronic devices - Recycling | 49,7 | 93,4 | 31,4 |

| Paper and cardboard - Recycling | 128,5 | 206,6 | 233,5 |

| Metal scraps -Recycling | 45,4 | 114,1 | 76,4 |

| A) Total waste diverted from final disposal | 224 | 427,3 | 341,6 |

| Non-hazardous waste (Class II) - directed tod disposal | |||

| Co-processing | 0,3 | 1,5 | 0 |

| Waste directed to landfills² | 0 | 0 | 125,0 |

| B) Total waste directed to final disposal | 0,3 | 1,5 | 125,0 |

| Total generated waste in tons (A+B) | 223,9 | 428,8 | 466,6 |

1In 2022, we did not have vaults sent for recycling, with only the donation of these items for reuse. In this case, as it is a donation, they are considered in units in the item dealing with the donation of furniture.

2The organic solid waste generated in the organization is destined for public collection in the localities where the agencies are present. In the administrative headquarters building there is a company contracted to dispose of organic waste. Until 2021 there was no measurement of the amount of this waste generated.

| Waste generated by type and destination (units) | |||

|---|---|---|---|

| 2020 | 2021 | 2022 | |

| Hazardous waste (Class I) - directed to disposal | |||

| Lamps - Recycling | 1.652 | 2.060 | 2.734 |

| Tonners - Reverse logistics³ | - | - | 621 |

| A) Total waste diverted from final disposal | 1.652 | 2.060 | 3.355 |

| Non-hazardous waste (Class II) - diverted from disposal | |||

| Furniture donation - Reuse⁴ | 2.127 | 4.999 | 2.391 |

| B) Total waste diverted from final disposal | 2.127 | 4.999 | 2.391 |

| Total generated waste in units (A+B) | 3.779 | 7.059 | 5.746 |

3From 2022, we started to inform the data regarding tonners forwarded to reverse logistics

4The safes donated for reuse are added to this item.

The number of workers who are not employees and whose work is controlled by the organization amounts to 2,204, of whom four are supernumeraries and 2,200¹ are interns.

Most common workers are interns, whose contractual relationship is established through an integration agent called Center for Company and School Integration (CIEE, in Portuguese). Interns serve bank customers, act as cashiers, provide documents to customers and perform collection activities. They also provide supporting services to the branches and other Bank departments, manage the flow of bank bags, clear documents and control documents in the archives.

The methodology and assumptions used to obtain this indicator gather data from the internal database. The significant change in the number of workers is due to the duration of the internship contract, which is up to two years.

¹ The 2022 Administration Report shows 2,293 trainees. The difference is due to the criteria used in the consultation, which also included those who left during the month. After adjustments, those who left during the month were disregarded for the purposes of the Sustainability Report.

The ratio of the annual total compensation for the organization’s highest-paid individual to the median annual total compensation for all employees is 12.0%, while the ratio of the percentage increase in the annual total compensation for the organization’s highest-paid individual to the median percentage increase in the annual total compensation for all employees is 0.8%.

Annual salary increases occur in April (regulatory promotions retroactive to January) and in September (collective bargaining agreement).

For calculation purposes, the CEO, who is not a Bank employee, was considered as the highest-paid individual. The other workers who are not employees were not considered in the calculation. The total compensation (salaries, bonuses, job commission, full performance bonus, annual bonus, overtime, singing bonus, relocation bonus, management, retirement bonus, and retirement incentive) was considered in calculating compensation.

Banrisul operates in the public and private sectors. The Bank and its affiliates currently have several types of suppliers: lawyers; consultants; system analysts; sellers of perishable and non-perishable goods; international IT companies; armored truck companies; and numerous other service providers.

The number of direct suppliers, in 2022, is estimated at 1,093. The Bank hires suppliers to provide services and products unrelated to its core activity, i.e., they provide supporting services and products, including security, cleaning, transportation of valuables, acquisition of IT systems, telephone and internet services, acquisition of furniture, building rental, acquisition of sundry items.

Banrisul acts as a financial agent for customers, from industry, agriculture, transport, service, trade and health sectors. Most of them are located in Brazil’s South region.

Stakeholder categories with whom Banrisul engages are:

- Employees;

- Shareholders/investors;

- Market analysts;

- Customers;

- Suppliers;

- Government;

- Unions;

- Executive Board;

- Board of Directors;

- Social, Environmental and Climate Responsibility Committee – CRSAC.

The Institution has identified the need to create a stakeholder engagement program to strengthen its relationship with these groups and provide greater business opportunities and chances to listen to them. The goal is that this program enables the Institution to explore relationship channels with several groups.

For preparing its materiality, Banrisul surveyed all its target audiences, creating an opportunity to get to know their interests.

| Average training hours per employee, by gender | ||||

|---|---|---|---|---|

| Gender | 2020 | 2021 | 2022 | Δ 2021/2022 |

| Men | 37.1 | 45.7 | 67.0 | 46.5% |

| Women | 32.4 | 42.7 | 65.3 | 52.9% |

| Total training hours | 34.5 | 47.3 | 66.1 | 39.9% |

| Average training hours per employee, by employee category | ||||

|---|---|---|---|---|

| Employee category | 2020 | 2021 | 2022 | Δ 2021/2022 |

| Superintendent | 14.3 | 20.3 | 44.4 | 118.5% |

| Manager | 59.6 | 57.5 | 114.7 | 99.5% |

| Analyst | 11.9 | 29.7 | 39.6 | 33.3% |

| Assistant | 11.4 | 19.6 | 31.3 | 59.7% |

| Without commissioned position | 33.6 | 38.8 | 64.3 | 65.7% |

| Interns | 16.8 | 36.4 | 55.8 | 53.4% |

| Other | 78.7 | 31.1 | 66.0 | 112.1% |

Card-related losses incurred in the reporting period totaled R$1.8 million.

The Chair of the Board of Directors is not the Company’s CEO.

100% of employees are covered by collective bargaining agreements.

In compliance with Law 13,303/16, every year, elected Management members attend specific training on corporate and capital market legislation, disclosure of information, internal controls, code of conduct, Law 12,846, of August 1, 2013 (Anti-Corruption Law) and other topics related to the activities of a publicly held company or government-controlled company. In 2022, ESG was included in the list of topics. Additionally, Management members may participate in other courses/events with themes pertinent to their responsibilities in the respective governance bodies, if said theme is interesting for the Company.

The Business Partnership and Open Banking Department has been working constantly with Bem Promotora on the Prevention of Money Laundering and Terrorist Financing (PLDFT, in Portuguese). In September 2022, Banrisul published its New Policy on Prevention of Money Laundering, Terrorist Financing and the Distribution of Weapons of Mass Destruction, which is a mandatory reading for all those operating the corresponding assets. This document was read by 1,440 operators.

Suspicions or evidence of non-compliance with Banrisul’s Code of Ethics and Conduct, policies, standards and institutional regulations in force should be reported through the Whistleblowing Channel, which allows the anonymous reporting of the misconduct, ensuring the right to confidentiality and protection against retaliation. The internal and external channels are available, respectively, on the Corporate Intranet and on Banrisul’s website (www.banrisul.com.br) and are intended for receiving misconduct reposts and complaints from employees and other stakeholders. The Control and Compliance Department is the independent area responsible for managing this channel.

Every six months the Board of Directors reviews a report on Banrisul’s Whistleblowing Channel. In compliance with article 3, paragraph 2, of CMN Resolution 4,859/2020, the Control and Compliance Department prepares a report with the following minimum information:

I – the number of reports received;

II – the nature of the reports;

III – the departments responsible for handling the situation;

IV – the average response time; and

V – the measures adopted by the Institution.

In 2022, there were 1,085 significant instances of non-compliance with laws and regulations, of which only one incurred in fine (one instance of irregular waste disposal). 720 Municipal Tax Unit (UFM, in Portuguese) (R$3,554.06) repaid by the outsourced cleaning company (as set forth in the contract) and other non-monetary penalties. Out of the 1,084 administrative or judicial proceedings that did not incur in fines, 1,082 are social in scope: six are events related to accessibility, 20 to over-indebtedness, one to customer moral harassment, 1,055 are labor complaint events (according to CMN Resolution 4,943/21), one environmental event (disposal of recyclable waste in an organic waste container), one climate-related event (collection lawsuit to recover the amounts from the plaintiff’s property insurance policy, affected by a storm).

Additionally, Banrisul received 262 notifications in this reporting cycle, 45 of which were fines for instances of non-compliance with laws, and all of these were paid during previous reporting periods.

Strictly speaking, the Bank did not identify incidents of corruption in the form of offering or requesting of undue advantages. Banrisul did not terminate or refuse to renew contracts due to the involvement or possible involvement of a correspondent in corruption. Neither the Organization nor its employees are parties to corruption-related lawsuits.

Banrisul’s Board of Directors identifies and manages conflicts of interest based on, but not limited to, applicable legal standards provided for in Article 156 of the Brazilian Corporate Law and article 25 of its Bylaws. Furthermore, the Code of Ethics and Conduct is widely disseminated to management members, board members, employees, interns, members of the Banrisul Group, business partners, suppliers and service providers. In the event of a potential conflict of interest, members of the Board of Directors, the Audit Committee and the Ethics Committee must abstain from resolving on matters in which this conflict is identified. Another important document governing this topic is the Related-Party Transactions Policy that outlines the conditions credit transactions and other related-party transactions.

The item “SUBORDINATION, SERVICE OR CONTROL RELATIONSHIPS BETWEEN THE ISSUER’S MANAGEMENT AND ITS SUBSIDIARIES, AFFLIATES AND OTHERS” of the Company’s Reference Form informs the interest held by Banrisul management in management of other companies in the Banrisul Group. The only controlling shareholder is the State of Rio Grande do Sul.

Related-party transactions, as well as measures taken by Banrisul, can be found in Note 29, pages 118 and 119, to the 2022 Financial Statements, available here.

The Control and Risk Executive Office is responsible for managing the Institutions’ corporate risks.

As regards Integrated Capital and Corporate Risk Management, the Chief Risk Officer (CRO) is responsible for the Corporate Risk Management Department and his/her duties include ensuring that the risk process monitors, controls, evaluates and plans capital need and goals and identifies, measures, monitors, reports, controls and mitigates credit, market, IRRBB, liquidity, operational, social, environmental and climate risks associated with the Prudential Conglomerate, communicating said risks to the Risk Committee, the CEO, the Board of Directors and regulatory agencies.

The Corporate Risk Executive Superintendent reports to the CRO on the Institution’s risk management. At least every year, risk management reports are submitted to the Board of Directors for consideration.

At Banrisul, the analysis of credit risk is carried out through statistical models for individuals and for the mass corporate segment, which comprises companies with average monthly income of up to R$2 million that do not belong to economic groups and/or exceptional segments.

The exceptional segment is identified based on the company’s main activity in the national classification of economic activities (CNAE, in Portuguese) and includes companies that have atypical cash flows, as well as those that are not targets of Banrisul’s market of interest.

In the segments with little commercial interest, we list the segments with high environmental and social risk. Companies that are not subject to the mass analysis are analyzed on a case-by-case basis observing quantitative and qualitative aspects.

The Bank currently checks with external agencies whether the customer, either an individual or a company, has been listed as an “Employer that uses Forced Labor” or as causing “Environmental Damage” (conviction for environmental damage in actions filed by Brazil’s environmental protection agency (IBAMA, in Portuguese)). Potential new customers identified as an “Employer that uses Forced Labor” are not allowed to obtain credit of any type. If existing customers are included in this list, Banrisul takes specific measures to discontinue the business relationship. The occurrence of environmental damage, on the other hand, prevents customers from obtaining specialized credit lines.

Regarding social aspects, there are markings in the Risk Calculation and Negative Occurrence systems indicating individual customers classified based on a proprietary model to identify vulnerabilities, in which customers with a high score go through a special credit granting process, with the application of regulations to product policies. In addition, the credit granting guidelines define the overall limits that should be considered in the process, preventing over-indebtedness.

Moreover, in larger transactions, especially those involving larger companies or exceptional segments (for which we do not set limits using a mass model), Banrisul carries out a case-by-case analysis using data from the financial statements, notes to the financial statements and other information, in addition to requiring the filling out of a specific checklist to learn more about the customer, helping analysts obtain qualitative information that will be used in their report and risk analysis, as well as in the definition of the exposure limit.

In order to include a qualitative aspect in credit analysis, Banrisul incorporated an ESG assessment tool into the process. The tool uses a questionnaire completed by companies/economic groups with exposure or proposed risk limit higher than R$5 million to generate a score that is incorporated into the customer’s internal risk rating. It is being used to assess the risk limit of sectors considered to be more sensitive to ESG aspects. ESG aspects are analyzed qualitatively by credit risk analysts in line with Banrisul’s Institutional Manual/Social, Environmental and Climate Policy.

The risk analysis for the establishment of the exposure limit is general in nature, i.e., it addresses the most relevant information and considerations for credit risk without taking account the specific characteristics of the credit lines in question. In this context, additional information and analyses can be required during the credit analysis and approval process, with special attention to ESG aspects, especially credit lines for investment, agribusiness and real estate projects.

Given the relevance of credit exposures, all the transactions above R$10 million in which the allocation of funds or credit granted is known are subject to the completion of standardized questionnaires to better measure the social, environmental and climate risk. This questionnaire may also be used in other transactions or in transactions involving a lower amount.

The guidelines related to the products, which complement the Institution’s Credit Policy, are set out in the specific regulations for Agribusiness (N7), Development (N33) and Real Estate (N30).

In order to estimate credit losses during the duration of the contract of the financial assets, the provision for credit losses is calculated monthly for all active contracts based on the rating calculation. Currently, the credit rating of Banrisul’s credit transactions can be hurt if the client does not have an approved credit exposure limit. For some industries, this individual analysis to determine exposure limit is forbidden, for example sectors/CNAE of gambling and betting, several agricultural crops (such as tobacco and sugar cane).

In the context of the Stress Test Program, the scenario is assessed in two stages. At first, the accounting balance of the adverse scenario is used in the ad hoc scenario analysis. All transactions classified as highly exposed to climate risk are downgraded by one level of risk, resulting in a higher provision. The difference between the new provision and the initial provision is then added to the amount of the expected difference between the loss in the adverse scenario and the loss in the credit base scenario.

These data are sent to the budget department, which will calculate the income statement with these new provision amounts, attesting to the Institution’s resilience in the face of a possible stress. Whereas the individualized analyses make use of, but are not limited to, relevant information from the ESG agenda, the knowledge acquired during these analyses, combined with the constant monitoring of trends, is how we currently seek to identify opportunities for improvements in our processes.

As we monitor the credit portfolio, we look at credit allocation according to the sector, as well as the largest individual and economic group exposures. In the geographical context, the statistical models used in credit granting include a variable that indicates the main regions of the state.

The Green Taxonomy (Brazilian Federation of Banks — FEBRABAN, in Portuguese) is used to analyze the risk exposure profile. The assessment is based on the borrower’s code in the National Classification of Economic Activity (CNAE) in three dimensions: Contribution to the Green Economy, Exposure to Climate Change and Exposure to Environmental Risk.

The activities listed in Resolution 237/97 of the National Environmental Council (CONAMA, in Portuguese), which requires environmental licensing for sectors with higher potential impact, were considered in the classification of the Exposure to Environmental Risk. In December 2022, 41.49% of the corporate credit portfolio had high exposure to environmental risk.

The classification related to Exposure to Climate Change was prepared based on the activities defined by Task Force on Climate-related Financial Disclosures (TCFD) as having the highest probability of being affected by transition and physical risks considering three factors: greenhouse gas (GHG) emissions, energy use and water consumption. These sectors were classified as High Exposure, and the activities related to or financially exposed to this sector were classified as Moderate Exposure. In December 2022, 44.61% of the corporate credit portfolio had significant exposure to climate risk.

In addition to the credit risk assessment, the customer’s exposures are controlled to avoid over-indebtedness. Based on the client’s risk rating, size and profile, the Bank determines healthy income commitment levels (percentage of income allocated to debt servicing), as follows:

- For individuals: Overall Limits (OG) are defined to determine the client’s monthly income commitment level;

- For companies in the mass segment: the short-term monthly commitment (C), the Credit Limit (CL) and the Product Limits (PL – six product groupings according to homogeneous characteristics) are used to assess the client’s total exposure, including in the National Financial System;

- For companies analyzed on a case-by-case basis: the Risk Limit (RL) is defined separately between transactions with personal guarantee and security interest.

| Tons of CO2 equivalent p.a. | ||||

|---|---|---|---|---|

| Type of emissions | 2020 | 2021 | 2022 | △ 2022/2021 |

| Scope 1 (Direct emissions) | 639.7 | 958.9 | 728.3 | -24.0% |

| Scope 2 (indirect emissions) | 2,067.6 | 4,642.3 | 1,446.8 | -68.8% |

| Scope 3 (other indirect emissions) | 31.0 | 5,054.4 | 7,685.0 | 52.0% |

| Total emissions (Scope 1, 2 and 3) | 2,738.3 | 10,655.6 | 9,860.2 | -7.5% |

| Total Biogenic emissions of CO2 in Scope 3¹ | 13.8 | 900.3 | 1,463.4 | 62.6% |

| Other - HCFC 22 (R22) | 2,970.7 | 3,010.0 | 1,007.5 | -66.5% |

¹Considers scope 1 and 3 emissions

As for fugitive emissions, which are encompassed in Scope 1 emissions, Banrisul began a process to modernize its air conditioning equipment, in order to reduce fugitive gas emissions. In this sense, we believe it is already possible to see a slight reduction in fugitive emissions due to this program.

As for mobile combustion, Banrisul will change the fuel used by its proprietary and leased vehicle fleet to ethanol in 2023. The goal is to have the entire fleet using this fuel whenever available (given that not every gas station offers ethanol, especially when the vehicles are located in smaller cities), in order to reduce emissions from mobile combustion.

The reduction seen in emissions for reference year 2022 was due to a reduction in the reference conversion factor used by the GHG Protocol tool. In 2021, the average annual factor (tCO2/MWH) was 0.1264 and, in 2022, it was 0.0426, which explains the decrease in tCO2 equivalent emissions.

Measurement of Scope 3 emissions improved after one year. For the 2022 inventory, Banrisul included additional information in the Upstream Transport category, related to light ATM maintenance vehicles that were not included in the previous inventories. Similarly, cash and money deposit bag transportation increased significantly, in absolute number of liters of fuel used from 562,557 in 2021 to 986,962 in 2022, largely due to the gradual recovery of the economy after the pandemic.

There are no reduction targets defined, since the Bank intends to increase the number of categories included in the Scope 3, leading to an upturn in emissions.

Percentage of individuals within governance bodies by gender

| Gender | 2020 | 2021 | 2022 |

|---|---|---|---|

| Men | 85.0% | 90.0% | 88.1% |

| Women | 15.0% | 10.0% | 11.9% |

Percentage of individuals within governance bodies by age group

| Age group | 2020 | 2021 | 2022 |

|---|---|---|---|

| Under 30 years old | 0.0% | 0.0% | 0.0% |

| 30-50 years old | 32.5% | 27.5% | 26.2% |

| Over 50 years old | 67.5% | 72.5% | 73.8% |

Percentage of employees per employee category by gender

| Employee category | Gender | 2020 | 2021 | 2022 |

|---|---|---|---|---|

| Superintendent | Men | 70.1% | 66.2% | 66.7% |

| Women | 29.9% | 33.8% | 33.3% | |

| Manager | Men | 61.8% | 61.1% | 60.1% |

| Women | 38.2% | 38.9% | 39.9% | |

| Analyst | Men | 62.7% | 61.4% | 60.5% |

| Women | 37.3% | 38.6% | 39.5% | |

| Assistant | Men | 55.9% | 63.5% | 55.8% |

| Women | 44.1% | 36.5% | 44.2% | |

| Without commissioned position | Men | 51.2% | 50.2% | 49.7% |

| Women | 48.8% | 49.8% | 50.3% | |

| Interns | Men | 43.0% | 43.2% | 39.5% |

| Women | 57.0% | 56.8% | 60.5% | |

| Other | Men | 53.7% | 55.7% | 54.8% |

| Women | 46.3% | 44.3% | 45.2% |

Percentage of employees per employee category by age group

| Employee category | Age group | 2020 | 2021 | 2022 |

|---|---|---|---|---|

| Superintendent | Under 30 years old | 0.0% | 0.0% | 0.0% |

| 30-50 years old | 37.3% | 32.4% | 31.9% | |

| Over 50 years old | 62.7% | 67.6% | 68.1% | |

| Manager | Under 30 years old | 2.0% | 1.6% | 1.7% |

| 30-50 years old | 68.2% | 69.0% | 69.9% | |

| Over 50 years old | 29.9% | 29.5% | 28.4% | |

| Analyst | Under 30 years old | 2.0% | 2.0% | 2.1% |

| 30-50 years old | 61.7% | 65.3% | 66.2% | |

| Over 50 years old | 36.2% | 32.7% | 31.7% | |

| Assistant | Under 30 years old | 7.2% | 2.0% | 0.0% |

| 30-50 years old | 69.7% | 68.9% | 66.2% | |

| Over 50 years old | 23.0% | 29.1% | 33.8% | |

| Without commissioned position | Under 30 years old | 7.3% | 4.2% | 2.2% |

| 30-50 years old | 67.9% | 68.5% | 67% | |

| Over 50 years old | 24.8% | 27.3% | 30.8% | |

| Interns | Under 30 years old | 86.7% | 89.4% | 88.0% |

| 30-50 years old | 12.8% | 10.6% | 11.6% | |

| Over 50 years old | 0.5% | 0.1% | 0.4% | |

| Other | Under 30 years old | 1.8% | 0.5% | 0.5% |

| 30-50 years old | 59.8% | 57.1% | 57.4% | |

| Over 50 years old | 38.4% | 42.4% | 42.1% |

Employee percentage per employee category, by color or race¹

| Employee percentage per employee category, by color or race¹ | ||||

|---|---|---|---|---|

| Employee category | Color or race | 2020 | 2021 | 2022 |

| Superintendent | Black | 0.0% | 0.0% | 0.0% |

| Multiracial | 0.0% | 1.5% | 1.4% | |

| White | 100% | 98.5% | 98.6% | |

| Indigenous people | 0.0% | 0.0% | 0.0% | |

| Yellow | 0.0% | 0.0% | 0.0% | |

| Manager | Black | 1.4% | 1.5% | 1.8% |

| Multiracial | 2.1% | 2.1% | 2.6% | |

| White | 96.3% | 96.2% | 95.3% | |

| Indigenous people | 0.1% | 0.1% | 0.1% | |

| Yellow | 0.1% | 0.1% | 0.2% | |

| Analyst² | Black | 2.4% | 2.5% | 2.7% |

| Multiracial | 2.2% | 2.7% | 2.9% | |

| White | 94.9% | 94.4% | 94.1% | |

| Indigenous people | 0.1% | 0.1% | 0.1% | |

| Yellow | 0.3% | 0.3% | 0.2% | |

| Assistant | Black | 4.3% | 4.7% | 2.6% |

| Multiracial | 2.6% | 2.0% | 1.3% | |

| White | 93.1% | 93.2% | 96.1% | |

| Indigenous people | 0.0% | 0.0% | 0.0% | |

| Yellow | 0.0% | 0.0% | 0.0% | |

| Without commissioned position | Black | 2.3% | 2.2% | 2.0% |

| Multiracial | 3.2% | 3.0% | 2.7% | |

| White | 94.3% | 94.5% | 95.1% | |

| Indigenous people | 0.1% | 0.1% | 0.1% | |

| Yellow | 0.2% | 0.2% | 0.2% | |

| Other | Black | 2.4% | 2.2% | 2.3% |

| Multiracial | 2.8% | 3.2% | 2.9% | |

| White | 94.6% | 94.3% | 94.5% | |

| Indigenous people | 0.0% | 0.0% | 0.0% | |

| Yellow | 0.2% | 0.2% | 0.3% | |

¹Interns not are not included in this calculation.

²3 analysts chose not to report their race.

As part of its commitment to the material topic, Banrisul uses renewable energy. The Bank joined the Carbon Disclosure Project (CDP) and the Brazilian GHG Protocol program to enhance its technical and institutional capabilities to manage greenhouse gas emissions, including calculation and reporting.

Energy efficiency and ESG in the supplier chain: the Organization has committed to managing the topic, and the quality analysis is based on regulatory compliance with Federal Law 13,589/2018.

The appropriate mapping of these processes with definition of the destination of each type of waste generated goes beyond compliance with environmental legislation, embodying the Organization’s social and environmental commitment to the community where it is inserted, and the natural resources used.

To manage energy efficiency and ESG aspects in the supplier chain, ESG criteria are used in project design, construction works and engineering services (carried out by the Construction and Maintenance departments); air quality analysis; contract management conducted by the Maintenance department; and publication of certificates to users.

At Banrisul, waste is managed by the Sustainability department, administratively linked to the Property Management Unit. This department is responsible for defining processes related to the appropriate management of solid waste produced by the Organization and for internal decision-making processes, which are validated by specific committees, when necessary.

In order to prevent and mitigate negative and potential impacts, in 2028, Banrisul implemented a Solid Waste Management Plan (PGRS, in Portuguese), which describes and recommends the appropriate handling of waste and the routine procedures necessary to comply with the legal environmental requirements.

It also controls monthly waste generation and fills out mandatory Waste Transportation Manifests (MTR, in Portuguese) with information on the transported waste, as required by the state environmental protection agency (FEPAM, in Portuguese). For each destination, specific documents are generated, such as the Waste Transportation Manifest and, at the end of the operation, the Final Disposal Certificate (CDF, in Portuguese), presenting all the information related to the waste handled.

Waste disposal processes also include concerns about stakeholders, as the disposal of certain types of waste is linked to social impact projects, including working with convicts, in the case of the decharacterization of unusable furniture, or training of vulnerable persons, as in the destination of electronic waste, through the Sustentare project, led by the Rio Grande do Sul state government, in which Banrisul has been a partner since the beginning of the initiative.

Banrisul offers its internal public distance-learning programs on sustainability and waste management, as well as in-person lectures and informational campaigns on the intranet.

One of the points identified for improving waste management processes is the update of the Solid Waste Management Plan, which will enable a review of all the incorporated practices and determine if there are gaps to be closed, as this process is conducted by a consulting firm hired for this specific purpose.

Similarly, the Bank identified the need to make the most up-to-date version of the PGRS available to the entire internal public, as well as reinforce campaigns to spread knowledge on appropriate waste sorting practices.

As an example of positive feedback from a stakeholder related to the effectiveness of waste management, there is the destination of electronic waste to the Sustentare program of the Rio Grande do Sul state government, which partners with companies, entities and associations interested in reconditioning and/or recycling electronics.

The effectiveness of renewable energy use is tracked through regular reports presented to the Administrative Officer. Energy efficiency is tracked by monitoring energy consumption at Banrisul’s premises. The air quality analysis is based on reports issued by laboratories. ESG effectiveness in the supplier chain is tracked through the inspection of the works and services with the issuance of a technical monitoring report.

Banrisul transferred consumer units to the free energy market (ACL, in Portuguese) from October to December 2022. It also delivered spaces featuring energy-efficient components and equipment, such as occupancy sensors to turn lights on and off, LED panels, inverter air conditioning equipment and sunshades. For the air quality analysis, an air collection and analysis procedure is conducted every six months at Banrisul’s premises (including both units that do and do not serve customers). Waste generation is not constant at the Organization, which makes it difficult to establish individual targets.

The Bank identified the need to have a manager that has already been hired to monitor operational and support procedures in the issuance of reports and control and track the use of renewable energy and energy efficiency. Regarding air quality, it is necessary to monitor the publication of resolutions and standards issued by regulatory and supervision agencies.

The greenhouse gas mitigation plan is designed to reduce scope 1 and 2 GHG emissions and offset all remaining emissions with the annual carbon neutral project; maintain the air-conditioning equipment at the branches within its useful life (10 to 15 years) until 2030; and sustain improvements in eco-efficiency projects. Waste management is monitored through monthly waste volume indicators, which include individual controls for each type of waste.

| Impact | Classification (positive or negative) | Event (potential or actual) | Time frame (short-term or long-term) | Systemic or one-time impact | Irreversibility (high, medium, low - only for negative impacts) | Production chain process or activity that causes impact | Resources / stakeholder group impacted |

|---|---|---|---|---|---|---|---|

| Increase in the use of renewable energy | Positive | Actual | Short-term | One-time | - | During energy purchase. | Shareholders and Investors, Environment, Banrisul’s Operations. |

| Energy Efficiency | Positive | Actual | Short-term | One-time | - | By purchasing inputs and hiring suppliers | Shareholders and Investors, Environment, Banrisul’s Operations. |

| Incentive to ESG practices in the supply chain | Positive | Potential | Long-term | Systemic | - | In managing and operating outsourced contracts. | Shareholders and Investors, Employees, Customers, Suppliers, Environment, Banrisul’s Operations. |

The year 2022 was very important for the progress of the Diversity, Equity & Inclusion agenda, as this topic was internally institutionalized, and formal Governance mechanisms were introduced to move this work forward. To ensure diversity and collaboration that this topic requires, Banrisul created three initial Affinity Groups: Gender Equity, whose main goal is the pursuit of gender equity; People with Disabilities, with the main purpose of fostering the inclusion of colleagues with disabilities; and Race, whose goal is to promote racial equity.

To support and coordinate these Affinity Groups Banrisul created a Diversity, Equity & Inclusion Committee, composed of members from various backgrounds and the Affinity Groups’ coordinators, ensuring the necessary diversity and representativeness to address the agendas. The diversity indicators are still being developed to provide the grounds to monitor related impacts.

| Impact | Classification (positive or negative) | Event (potential or actual) | Time frame (short-term or long-term) | Systemic or one-time impact | Irreversibility (high, medium, low - only for negative impacts) | Production chain process or activity that causes impact | Resources / stakeholder group impacted |

|---|---|---|---|---|---|---|---|

| Bank’s reputation and image | Positive | Potential | Long-term | Systemic | - | Management of this topic within the Organization, from the public service exam to the termination of the employment contract. | Shareholders and Investors, Employees, Community, Customers, Suppliers, Banrisul’s Operations. |

| Increase in the share of minority groups in the Organization and in leadership positions | Positive | Potential | Long-term | Systemic | - | Management of this topic within the Organization, from the public service exam to the termination of the employment contract. | Shareholders and Investors, Employees, Banrisul’s Operations. |

| Greater employee awareness of this topic | Positive | Actual | Long-term | Systemic | - | Management of this topic within the Organization, from the public service exam to the termination of the employment contract. | Shareholders and Investors, Employees, Suppliers, Banrisul’s Operations. |

| Development of more humane and inclusive management | Positive | Potential | Long-term | Systemic | - | Leadership development | Employees, Customers, Banrisul’s Operations. |

The management of this topic started with the structuring of the Data and Analytics Management department, in 2019, and included the appointment of the Data Protection Officer (DPO), who is responsible for conducting internal activities to ensure compliance with the General Data Protection Act (LGPD, in Portuguese) and serve as a focal point between the Organization, the holders of personal data and the National Data Protection Authority (ANPD, in Portuguese).

The Data Privacy and Protection Governance Program was created to mitigate potential negative impacts. As part of the Program, a quarterly report is sent to the Internal Audit for compliance reporting. The Program covers several fronts, including:

• Mapping of all activities involving personal data processing, identifying the data life cycle, from collection to deletion, as well as the appropriate legal framework;

• Creation of a customer service channel for holders of personal data, ensuring the full exercise of all the rights set out in the LGPD;

• Formalization in a Standard of a flow of adaptation of contracts with third parties for compliance with the LGPD, including the definition of a methodology to help identify the Processor x Controller x Joint Controllers and define the flow for indicating LGPD clauses for business and administrative contracts;

• Implementation of the Privacy by Design and Privacy by Default methodologies in order to ensure the privacy and protection of personal data in the design of new products and services;

• Creation of specific guidelines for handling or responding to security incidents involving personal data considering the requirements imposed by the LGPD in order to complement Banrisul’s existing Information and Cyber Security Policy; and

• Development of internal training for all the staff on the main points addressed by the Law and their impacts on the workplace, as well as creation of a website featuring content that helps disseminate a culture of data privacy and protection in the Institution.

In order to address the actual negative impacts, Banrisul has approved the reporting flow of data breach incidents and created Guidelines for Prevention and Response to Personal Data Incidents. These documents are designed to ensure the prevention of personal data incidents related to Banrisul and its customers, including the means/processes that should be implemented to mitigate and/or remedy any adverse impacts thereof, as well as appropriately respond to and deal with these incidents.

To track the effectiveness of the actions, quarterly reports are made to the Audit Committee and information is provided to any internal audits. The Bank organizes an annual calendar of activities of the Data Privacy and Protection Governance Program, covering all the goals and targets for the period.

The plan is designed based on the Regulatory Agenda of the National Data Protection Authority and best market practices, taking into account sustainability aspects.The annual plan of the Privacy and Data Protection Governance Program defines indicators, which, after approved by the Executive Board, are submitted to and monitored by the Strategy and Planning department. The Program runs continuously.

Management approach

| Impact | Classification (positive or negative) | Event (potential or actual) | Time frame (short-term or long-term) | Systemic or one-time impact | Irreversibility (high, medium, low - only for negative impacts) | Production chain process or activity that causes impact | Resources / stakeholder group impacted |

|---|---|---|---|---|---|---|---|

| Incidents with customers’ and employees’ personal data | Negative | Actual | Short-term | Systemic | Medium | In the activities or database that uses customer personal data, in the event of a failure in data security systems. | Shareholders and Investors, Customers, Banrisul’s Operations. |

| Process credibility and credibility and sharing personal data | Positive | Actual | Short-term | Systemic | - | In information flow controls, through the preservation of confidentiality and integrity of information. | Shareholders and Investors, Employees, Customers, Suppliers, Banrisul’s Operations. |

| Greater autonomy for the holder to control personal data | Positive | Actual | Short-term | Systemic | - | Information availability, protected at all times, kept complete and available only to those entitled to access it. | Shareholders and Investors, Employees, Customers, Suppliers, Banrisul’s Operations. |

| Greater transparency as regards access and use of personal data | Positive | Actual | Short-term | Systemic | - | Availability and authorization to use the information only to those entitled to access it. | Shareholders and Investors, Employees, Community, Customers, Suppliers, Environment, Banrisul’s Operations. |

| Loss of market and competitiveness due to information security incidents | Negative | Potential | Short-term | One-time | Medium | Maintenance of Information Security. | Shareholders and Investors, Employees, Customers, Suppliers, Banrisul’s Operations. |

As of 2021, Banrisul has adopted a manual that establishes sustainability criteria for procurement and bidding processes. This tool enabled the inclusion in the Organization’s procurement flow of product and service analyses related to the evaluation of the inputs used in production. As for the upstream chain, in 2022, Banrisul issued the Supplier Manual, a document with general guidelines on the Institution’s relationship with suppliers and a chapter dedicated to environmental responsibility, including guidelines on appropriate waste management at the supplier, always in compliance with the current environmental legislation.

Waste generated by Banrisul’s own activities came into the spotlight as of 2001, with the launch of the Reciclar (Recycle) program, designed to encourage and promote the environmentally friendly collection and final disposal of the waste generated by the Institution, seeking to reduce the negative environmental impact of its activities.

On the other hand, in order to reduce the generation of single-use plastic waste, Banrisul implemented Copinho Zero (Zero Cups), a project designed to encourage all employees to replace plastic cups with reusable coffee mugs and water bottles. Banrisul also has a project to streamline back-office operations in its branches with the aim to reduce the volume of paper used in the issuance of reports. Safes that are no longer used by the Institution are donated so that they can be reused. If this is not possible, they are decharacterized, and the resulting material is recycled or reused.

Electronic waste generated by the branches and units is sent to the Sustentare/RS Program, with three possible destinations: donation, reconditioning and recycling. In order to appropriately handle the furniture that the Institution no longer uses, Banrisul donates these items to non-profit institutions interested in reusing them. Banrisul also disposes of fluorescent lamps in an environmentally friendly manner by sending these components to a company hired for this purpose. In 2022, 2,734 fluorescent lamps were sent for recycling. There is also reverse logistics for materials such as batteries, structured cables and printer toner refills.

The organic waste generated by the Organization is sent for public collection in the locations where the branches are located. The waste generated by the Organization is centrally managed by Banrisul through the Sustainability Department, in particular, the waste management unit, which is responsible for managing contracts related to waste and for the receipt, temporary storage and environmentally friendly disposal of waste, through partners duly hired to handle each type of waste. Waste sent for disposal is controlled through the issuance of Waste Transportation Manifests (MTR, in Portuguese) and Final Destination Certificates (CDF, in Portuguese). All the waste destined for the Bank’s waste management is measured quantitatively through control spreadsheets and later appropriately disposed of according to the type of waste. The waste disposal is demonstrated through the issuance of Waste Transportation Manifests and Final Destination Certificates.

At Banrisul, credit risk analysis is based on statistical models for individuals and for corporate customers in the retail segment. Corporate customers in the retail segment include companies with average monthly revenue of up to R$ 1 million, which do not belong to economic groups and/or exception segments.

The exception segment is identified based on the company’s main National Registry of Economic Activity (CNAE – Cadastro Nacional de Atividade Econômica). This group includes companies that have atypical cash flows with seasonal periods, as well as those that are not targets of Banrisul’s market of interest. In the segments with low commercial interest, the Bank has listed those with high environmental and social risk.

Legal entities that are not subject to the retail analysis are also analyzed on an individual basis, in which quantitative and qualitative aspects are observed. In the qualitative analysis, besides the governance and management aspects, which are essential for credit risk analysis, environmental and social matters related to the company and its production chain are evaluated. These analyses are performed by risk analysts, who are arranged in specialized groups per sector in which the companies operate, who interact with each other and have an in-depth knowledge of the companies, their role and impact on the local economy – a situation that provides an opportunity for a better identification of possible risk factors and atypical behavior by some companies. Also, for large corporations, risk assessment is carried out based on specific qualitative aspects for approaching ESG topics, which result in a classification that takes into account these aspects without being limited to them.

The retail risk analyses are carried out based on the information recorded in our registration, billing, and incident reporting (BLT in Portuguese) systems. The BLT system gathers have internal and external incidents received from credit bureaus and other official bodies, registering managerial and restrictive incidents that may indicate the worsening of risk from the ESG perspective, among them is forced labor and environmental damage, both considered as impediments to credit assignment. As for individual analyses, in addition to these same controls, data extracted from the financial statements and notes thereto, as well as other information made available by customers are used. They must also fill out a specific checklist, which helps analyst to gather qualitative information that will be used in their opinion, including risk analysis and exposure limits.

Risk analysis for the formation of exposure limit is generalist, that is, it addresses the most relevant information and considerations for credit risk without yet considering the specific characteristics of the credit that will be contracted. Within this context, additional information and analyses may be requested during the analysis and operations are approved observing ESG aspects, with special relevance for investment lines, agribusiness and real estate ventures.

Given the relevance of credit exposures, all operations above R$10 million in which the use of funds or directed credits is known must fill out a questionnaire (Formulário Normatizado Modelo 1.31000.01). The questionnaire may also be applied to other operations or amounts lower than this threshold.

Allowance for loan losses (PCLD in Portuguese) is calculated monthly for all active contracts based on the rating calculation. Currently, the customer not having an approved credit exposure limit is one of the factors that can worsen the rating classification of Banrisul’s credit operations. For some industries, this individual analysis to determine exposure limit is forbidden, for example sectors/CNAE of gambling and betting, several agricultural crops (such as tobacco and sugar cane).

Moreover, the analysis of denials of exposure limits may occur due to the lack of environmental licenses, debts with the union, and one of the consequences is the possibility of worsening the rating classification, especially for customers who already have exposure with the Bank.

Furthermore, regardless of the exposure limit in force and the size of the company or individual customer, in the monthly calculation of the Allowance for Loan Losses, incidents are verified that may worsen the customer’s risk in a timely manner, such as inclusion on the Forced Labor list, Court Restrictions, internal audit notes for fraud, fraud with the Bacen and irregularities with the Brazilian Securities and Exchange Commission.

ESG aspects are assessed qualitatively by the credit risk analysts and the evaluation is in line with Banrisul’s Institutional Manual/ Social and Environmental Responsibility Policy.

Considering that the individual analyses rely on relevant information from the ESG agenda, but are not limited to it, the experiences gathered in the course of these analyses, together with the ongoing monitoring of trends, are currently how the institution identifies opportunities for improvement in our processes.

In monitoring the credit portfolio, Banrisul has viewed credit allocation according to the sector in which the customer operates, as well as the largest individual exposures and those of economic groups. These views are shared with various Banrisul units, contributing to timely initiatives that may lead to adjustments in the automated exposure limits – an action carried out with greater recurrence during the pandemic, in individual analysis of the exposure limits (LR), in adjustments to the parameters of Allowance for Loan Losses calculation or in the worsening of the company’s risk rating – via individual analysis (monitoring) .

In the geographic context, the statistical models used in credit assignment have a variable that signals the main regions of the state where the information is gathered by the customer relationship branch, which, together with the CNAE (corporate customers) or CBO (individuals) information, add to and complement this sector and geographic evaluation.

In addition to the statistical models used for credit risk assessment, which aim at mitigating the risk of default and supporting the credit assignment process, the customer’s exposure is controlled in order to avoid over-indebtedness, which, based on the customer’s risk rating, size and profile, seeks to outline healthy levels of commitment, such as:

– For individuals, Global Limits (LGs) are outlined that mark the level of monthly commitment of the customer’s income;

– For corporate customers in the retail segment, there are the short-term monthly commitment (C), the Credit Limit (LC), and the Product Limits (LP – grouping of products according to homogeneous characteristics) – assessing the customer’s total exposure, including in the National Financial System;

– For legal entities that have individual analysis: Risk Limit (LR) is defined divided between operations with personal guarantees and those with real guarantees.

Also, statistical models are used for individual customers to classify the levels of vulnerability. Vulnerability is assessed in order to mitigate the risks related to the customer’s understanding (or lack of understanding) regarding products and services, as well as the risk of over-indebtedness. In order to qualify the service to customers with higher risk arising from their vulnerabilities or classified at a high level of vulnerability, their credit operations are analyzed exclusively by a higher committee.

In relation to customers who are circumstantially in financial vulnerability, the Bank has specific conditions and credit lines to readjust their financial flows, aiming to preserve Banrisul’s interests – both in receiving the credits granted and in satisfying the customer’s interest – to reorganize their flows and readjust their responsibilities to the Bank.In addition to these customer-focused aspects, the business areas make products focused on sustainability available. There is also a specific policy that establishes criteria for the acceptance of guarantees, which are aligned with the best market practices.

Banrisul is committed to investing in the regional culture and development, therefore, it seeks to support cultural and sports projects in the state’s different regions. Projects are assessed considering their relationship with regional development and their practical extension in several social aspects. These initiatives impact the local community through the economic development and accessibility improvements and contribute thought the preservation of tangible and intangible cultural heritage, in addition to fostering Rio Grande do Sul’s innovation ecosystem. As regards sports and education, projects offer better access to education, encourage young people and children to take up sports and contribute to fostering citizenship, human development and respect for equality in the population of Rio Grande do Sul.

Initiatives to improve the access to financial services for disadvanteged people

| Target disadvantaged group | Degree to which it is applied across the Institution | Progress made towards the initiative |

| Persons with disabilities | Process of mapping and improving the granting and renewal of technical opinions, declaring the correct application of pertinent to Architectural Accessibility of the buildings, in the case of Banrisul Branches, mainly in compliance with NBR 9050/2000. | Process started at the end of 2021. |

| People with Visual Impairments | Development of improvement in the voice communication systems in all Banrisul's most recently acquired ATMs, complying NBR 15250/2005. | Process started in 2019 and is currently in approval phase |

| People with Visual Impairments | As of 2018, audio description resources have been applied to Banrisul Group’s main websites to allow accessibility in compliance with the Brazilian Inclusion Law, SARB 01 - W3C Accessibility. | The description of images is already mandatory when posting pictures on the websites of Corretora de Valores, Consórcio Banrisul, BAGERGS, Novo seja Vero, Banricard and the Promotional Website. This is being implemented on the Banrisul Portal. |

| Persons with Disabilities | Since 2014, the Bank has continued to install the Accessible Desk, which is adapted/lowered furniture for priority/preferential service in all Banrisul branches, especially designed for wheelchair users or people with dwarfism. Compliance with Decree Law 5296/2004. | Monitored in 2021, in compliance with the regulation. |

| People with hearing impairments | Since 2008, Banrisul has trained employees to ensure they know the Brazilian Sign Language (Libras) to provide services to deaf and hard of hearing customers in its branches. The initiative complies with current regulations. | In 2021, the Bank recorded 1,296 trained employees, seeking to have at least two employees that know Libras at each of its branches. |

| People with Visual Impairments | As of 2018, Banrisul started to make the Debit and Credit Card Kit available to all its visually impaired customers. In addition to the traditional plastic card, the kit has information in Braille System and in Enlarged Font. | Every visually impaired customer duly registered at BAL already receives the card with tactile or visually enlarged accessibilities. More than 2,000 debit cards have already been issued from a base of about 1500 customers. |

| Persons with Disabilities | In 2014, the Bank launched the Accessibility distance learning program geared towards informing about the people with disabilities group and informing the staff about the best service practices and resources that can be offered to people/customers with disabilities or reduced mobility at Banrisul, with the aim of ensuring the inclusion of this public in the banking universe. The program seeks to comply with the regulations on Priority Service. | Approximately 30% of active employees had already taken the course in 2021. |

| People with visual impairments | The Banrisul Digital app has been following all the rules and development protocols to ensure accessibility to people with visual impairments, complying with SARB 01 and best market practices. | The Banrisul Digital Application is being developed so that all the services that have been or will be implemented have 100% accessibility in both IOS and Android systems. |